.png)

This week in crypto feels like an industry that has finally remembered what it felt like to have momentum. Bitcoin pushed to US$82,305 (AU$128,400), its highest level since January 31, and for once the price move has a credible story behind it. Progress on a US-Iran peace deal sent oil crashing, easing the inflation pressure that had been keeping the Fed's hands tied, and the market responded by leaning forward. Underneath the price recovery though, the week had a more complicated texture. Michael Saylor quietly broke one of crypto's most sacred rules. The White House put a date on the Clarity Act and at Consensus Miami 2026, Wall Street stopped asking what blockchain is and started asking how to build on it. The signal is getting clearer, even if not everyone is ready to admit it yet.

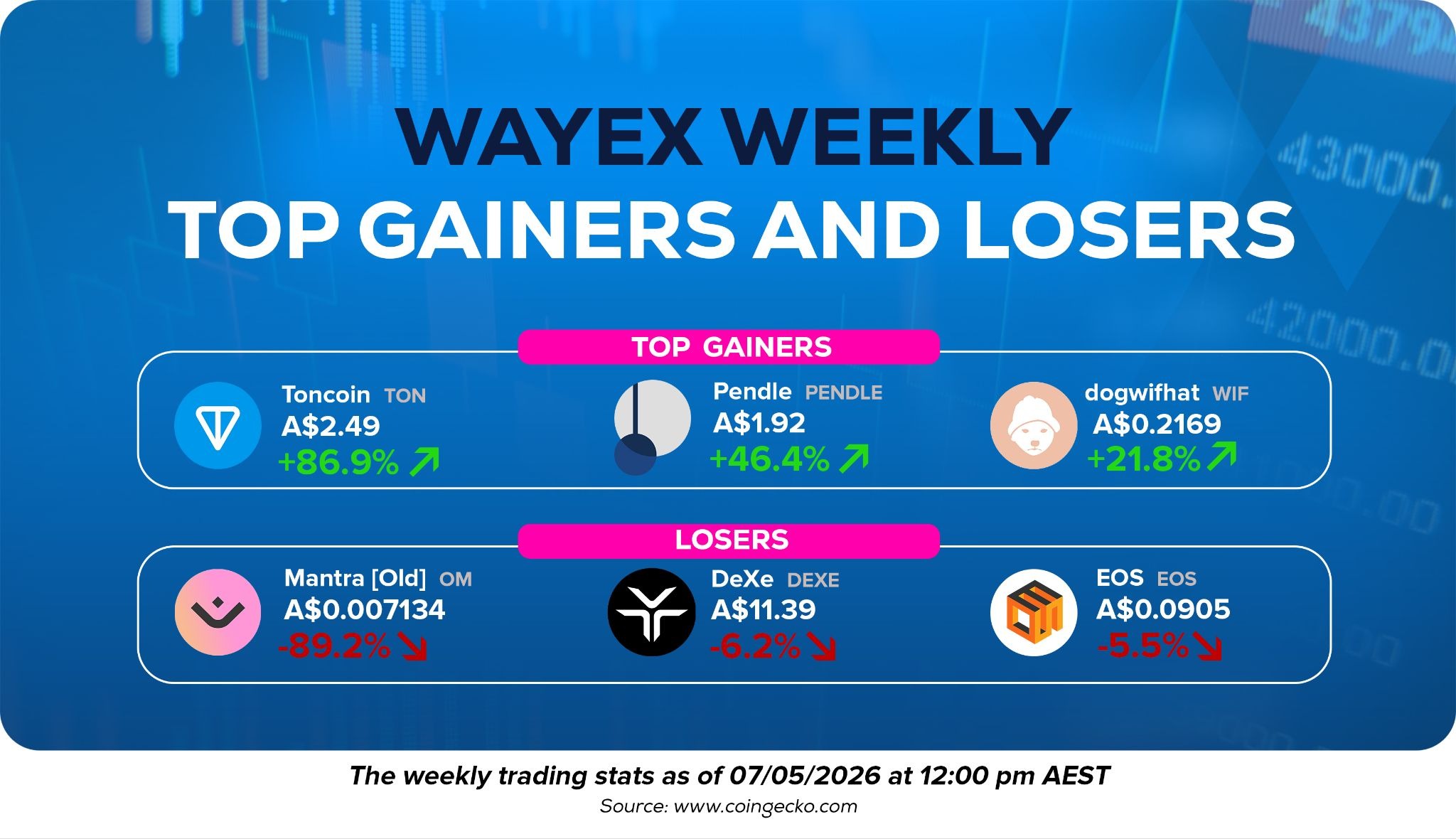

Top Gainers & Losers This Week

The Market Is Back, And It Means Something

Bitcoin pushing to US$82,305 (AU$128,400) this week is the kind of move that deserves more than a passing mention. This is not a dead cat bounce or a leverage-driven spike that evaporates in 48 hours. The catalyst was real: progress on a US-Iran peace deal sent oil prices crashing roughly 6%, easing the energy-driven inflation pressure that had been giving the Fed its most convenient excuse to hold rates. When the macro headwind shifts, risk assets move, and Bitcoin moved with conviction.

What makes this week's recovery more interesting than previous false starts is what is sitting underneath it. Spot Bitcoin ETFs recorded three consecutive days of inflows totalling more than US$1.16 billion (AU$1.81 billion), led by BlackRock's IBIT and Fidelity's FBTC. April's total ETF inflows came in at US$1.97 billion (AU$3.08 billion), the strongest monthly figure of 2026. That is not momentum built on retail speculation. That is institutional allocation continuing to compress Bitcoin's tradeable float at exactly the moment geopolitical relief gave the market room to breathe.

The honest caveat is that funding rates across major perpetual futures markets have remained negative, which historically signals the rally lacks the broad conviction needed for a clean breakout above resistance. Polymarket puts the probability of Bitcoin hitting US$90,000 (AU$140,600) in May at just 23%. The market is back. Whether it stays back is the question everyone is watching.

Is Strategy Getting Cold Feet?

For years, Michael Saylor made "never sell" the closest thing crypto had to a religious commandment. Strategy built its entire identity, its market premium, its institutional narrative, its cultural cachet on the idea that Bitcoin was a one-way accumulation play with no exit. This week, that changed. During Strategy's Q1 2026 earnings call, Saylor confirmed the company will probably sell some Bitcoin to fund dividend obligations on its preferred stock instruments, saying the move would serve to "inoculate the market" and prove the company can meet its commitments without stress.

The context matters. Strategy reported a US$12.54 billion (AU$19.6 billion) net loss for Q1 2026, driven largely by a US$14.46 billion (AU$22.6 billion) unrealised hit on its digital asset holdings. The company holds 818,334 BTC at an average cost of US$75,537 (AU$117,900) and faces approximately US$1.5 billion (AU$2.34 billion) in annual dividend obligations across its preferred stock instruments. Saylor's framing was deliberate: this is not a capitulation, it is a treasury operation. Buy with credit, let it appreciate, sell selectively to service obligations. The model is consistent with the original thesis, even if the optics of it land awkwardly.

The Bitcoin market barely flinched, with BTC slipping briefly below US$81,000 (AU$126,500) before recovering. The more important signal is what it tells you about the maturing corporate Bitcoin playbook. Pure accumulation with no liability management was always a thesis that worked best in a rising market. Strategy is now being asked to manage a balance sheet, not just a conviction call. That is a different, and considerably more complex, thing to do.

Coinbase Is Cutting Jobs, And AI Is Holding the Scissors

Coinbase announcing a round of employee cuts this week would have felt more surprising twelve months ago. The company is heading into earnings after a rough stretch for crypto markets, and the job reductions are being framed around AI efficiency gains rather than financial distress. The distinction matters, but it does not make the headline any less pointed. One of the most prominent companies in the industry is telling its workforce that artificial intelligence is doing work that humans used to do, and that the headcount reflects that reality.

This is not a Coinbase-specific story. It is an early signal of something that will play out across the entire crypto industry over the next few years. The back-office functions, the compliance workflows, the customer support infrastructure that exchanges built out during the bull market hiring sprees of 2021 and 2024 are increasingly being compressed by AI tooling. The companies that scaled headcount fastest are now discovering that the efficiency argument cuts in both directions.

For Coinbase specifically, the timing adds an uncomfortable layer. The company is walking into an earnings report carrying the weight of a difficult market stretch, a job cut announcement, and the ongoing question of whether its core trading revenue model is durable enough to survive another prolonged period of reduced volatility. Brian Armstrong has been vocal about Coinbase's long-term ambitions extending well beyond trading fees. This week is a reminder that getting there requires some painful recalibration along the way. The market will be watching the earnings numbers closely.

The Regulatory Clock Is Ticking And For Once, That's a Good Thing

The Clarity Act has a date. Speaking at Consensus Miami this week, Patrick Witt, executive director of the President's Council of Advisors for Digital Assets, confirmed the White House is targeting July 4 for House passage of the bill, describing it as a "tremendous birthday present for America" on its 250th. The Senate Banking Committee markup is planned for this month, with four working Senate weeks in June pencilled in for floor passage. For an industry that has spent years watching this bill stall, stumble, and get pulled back from the finish line, having a specific date attached to it by a White House official is a different kind of signal.

The sticking point that had threatened to derail everything, stablecoin yield, appears to have reached a workable compromise. Witt confirmed the debate between banks and crypto firms is "closed," with the resulting language leaving both sides equally unhappy. His framing of that outcome was honest and worth quoting directly: "Crypto's unhappy, banks are unhappy, but they're both about equally unhappy, and so we know that we got the right compromise." When nobody is thrilled, you probably have a deal. The remaining live issue is conflict-of-interest language, with Democrats pushing for ethics restrictions and the White House insisting any rules apply across the board rather than targeting specific officeholders or their families.

The Brazil story this week adds useful global context. Brazil's central bank published Resolution BCB 561/26, which some outlets rushed to call a stablecoin ban. It isn't. What it actually does is prevent traditional electronic foreign exchange providers from using stablecoins on their back-end for cross-border transfers, essentially banning the "stablecoin sandwich" where cross-border flows look like fiat but are really running on-chain. Brazilian corporations can still send stablecoins internationally, as long as they use a regulated digital asset platform. The resolution reinforces the boundaries between fiat services and digital asset services rather than eliminating the latter. The global regulatory picture is getting more defined. The direction, while messy, is forward.

DeFi Is Still Bleeding

The DeFi recovery narrative took another hit this week. The sector is still working through the aftermath of a string of high-profile exploits that have collectively done more damage to user trust than any regulatory crackdown could. The Financial Times reported on the ongoing fallout, and the picture it paints is not a pretty one. Hundreds of millions in user funds lost, protocols scrambling to patch vulnerabilities after the fact, and a governance layer that continues to prove it is not equipped to handle the speed and scale at which attackers are operating.

The core problem is structural. DeFi was built on the promise of trustless, permissionless finance, and that architecture is genuinely powerful. It is also genuinely difficult to secure. The attack vectors have shifted from pure smart contract exploits to something more insidious: social engineering, compromised governance, and the manipulation of trusted insiders over months rather than hours. The Drift Protocol hack that we covered in previous weeks was a textbook example of this. It did not require breaking the code. It required breaking the people.

What the industry has not yet solved is the gap between the speed of innovation and the maturity of its security and governance frameworks. Every major hack that goes uncompensated, every governance failure that locks users out of their own funds, and every protocol that chooses to move fast over moving carefully is a direct cost to the broader adoption story. DeFi's promise is real. The infrastructure needed to make that promise safe for the next hundred million users is still being built, and this week was another reminder of how much work remains.

Wall Street Is Going On-Chain Quietly

The most significant conversation happening in crypto right now is not taking place on crypto Twitter (X). It is taking place in boardrooms, compliance departments, and technology teams inside the world's largest financial institutions. At Consensus Miami this week, Robinhood VP Nicola White put it plainly: there is not a single traditional finance company they have spoken to that is not actively thinking about blockchain integration. The conversation has shifted from "what is this" to "how do we build on it." That is not a subtle change. That is a fundamental repositioning of where the industry's centre of gravity is moving.

Morgan Stanley made the shift concrete this week, launching crypto trading services through its E*Trade platform with access to its 8.6 million retail clients. The pricing is competitive, coming in at 50 basis points per transaction against the 60 to 95 basis points charged by Coinbase, Robinhood, and Charles Schwab. For a 91-year-old Wall Street institution to enter the crypto trading market on price is a statement of intent that the industry should take seriously. This is not a bank dipping a toe in the water. This is a bank that has decided crypto access is now a standard part of the retail brokerage product suite.

The honest qualifier, and the Robinhood panel at Consensus was candid about this, is that institutional adoption is moving slower and is more fragmented than the industry expected. Legacy infrastructure, regulatory caution, and the sheer complexity of integrating blockchain rails into decades-old financial plumbing means this transition will take years, not quarters. The direction, though, is no longer in doubt. Wall Street is building on-chain. The question is not whether it arrives. It is who captures the most value when it does.

Founder's Corner

Two things stood out to me this week above everything else. The first is the Clarity Act finally having a date attached to it. July 4 is ambitious, and the industry has been burned by optimistic timelines before. But there is something different about a White House official standing on a stage at Consensus and naming the day. The stablecoin yield compromise is closed. The conflict-of-interest language is the last live issue. For the first time in a long time, the path to the finish line is visible, even if it is not guaranteed. For platforms like Wayex that have been building compliant, regulated infrastructure on the assumption that the rules would eventually arrive, that visibility matters enormously.

The second is Wall Street's on-chain moment. Morgan Stanley entering crypto trading this week is not a headline to scroll past. When a 91-year-old institution decides that crypto access belongs in a standard retail brokerage account, the addressable market for this industry changes shape. The platforms positioned to meet that moment are the ones that were built for it before it arrived. The noise this week was loud. The signal underneath it, regulatory clarity approaching and traditional finance committing to the rails, is the one worth paying attention to.

Things That Made Us Laugh

**All information in this article is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained herein shall constitute a solicitation, recommendation, endorsement, or offer by Wayex to invest, buy, or sell any coins, tokens, or other crypto assets. Any descriptions of Wayex products or features are merely for illustrative purposes. Past performance is not a guarantee or predictor of future performance. The value of crypto assets can increase or decrease, and you could lose all or a substantial amount of your purchase price. It is essential for you to do your research and due diligence to make the best possible judgement, as any purchases shall be your sole responsibility.